Top Comment

Letushavepeace offered a contra-take in an exchange in the comments: "The longest yield inversion in history" is a statement that only makes sense if we limit "history" to the period for which there is ample data. The period following the Civil War had a yield inversion that lasted - depending on what rate estimates you choose for the shorter vs the longer maturities - until 1880.

http://www.tomsargent.com/research/PSHS_Bayes.pdf

https://people.brandeis.edu/~ghall/papers/PSHS_Method_20230602.pdf

MWG: This is a great point and is something I planned to introduce in Part 2. Briefly, a yield curve inversion is ALWAYS a sign of restrictive monetary policy. The period from 1872-1880 is known as The Long Depression and was largely a function of the exceptionally tight monetary policy required to return the US dollar "greenback" to gold backing.

LetUsHavePeace: I appreciate your genuine tolerance for the fat kid in the back of the class who won't put his hand down. The question of Greenbacks was settled at the end of Grant's first term. He had it literally rammed through Congress before the new members were seated. Hence, the Crime of 73. There was no monetary policy or Long Depression. Prices fell and relative wages rose, and immigration from everywhere exploded. I wrote a piece for X that should be published today - April 30 - that tries to explain why the curve inverted because of Grant's successful campaign. https://twitter.com/LetUsHavePeace1/status/1785280240534560792

MWG: Thanks for the feedback. Unfortunately, I’m going to have to disagree with you. The 1870s was a period of exceptionally tight monetary policy driven by the Resumption Act, which returned the US to the gold standard over a four-year period. The Crime of ‘73 was the end of bimetallism, squashing an arbitrage between cheap silver from the Comstock mines in Nevada and the official price of silver. Unfortunately, Western farmers, in particular, primarily relied upon silver (lower denomination than gold) as a wealth storage mechanism and the subsequent decline in the value of their savings relative to their debts contributed to a wave of financial distress in Western states.

The Resumption Act can be thought of as a Quantitative Tightening analog, although at a much-accelerated rate, especially relative to the growth of the US population, which LetUsHavePeace correctly observes surged. This surge was not driven by American opportunity as much as it was driven by a resumption of Civil War delayed immigration and the rolling waves of civil and economic distress occurring across Europe in the aftermath of the German and Italian unifications and the Franco-Prussian War.

The New York Fed has a nice piece on the Long Depression, and I like their acknowledgment that it has yet to be resolved whether it was entirely a monetary effect or due to a breakdown in the marginal productivity gains brought by the introduction of steel, rail, and steam to the United States:

The hard money view, with advocates in both political parties, moved Congress in the opposite direction of easier money with the passage of the Resumption Act in January 1875. The act required the Treasury to retire Greenbacks (currency not backed by gold) and committed the government to reinstate the gold standard in four years.

So, was the Long Depression just the industrial revolution peaking, with little that the government could do to offset defaults on a huge quantity of bad investments? Or was it unusually long because Washington pursued a hard money policy in the midst of recession in its quest to reinstate the gold standard?

https://libertystreeteconomics.newyorkfed.org/2016/02/crisis-chronicles-the-long-depression-and-the-panic-of-1873/

The Main Event

The US economic surprise indices slipped quietly back into negative territory this week, making the case for disinflationary surprises a bit less controversial. While the general focus on inflation is tied to persistently sticky inflation, which hopefully we helped address last week, the “savior” of the inflation story on the short-term has been about recession and economic weakness. This week saw significant “progress” in this direction.

Not only did we see average hourly earnings come in weaker, the Conference Board’s “Jobs Hard to Find” vs “Jobs Plentiful” continued to deteriorate:

As we’ve highlighted many times, the Jobs Hard-Plentiful is one of many indicators that can be used to create a “modified” Sahm rule with fairly obvious conclusions. I will caveat that the halting nature of this lift from lows is somewhat unique in the history series and helps to understand the slow nature of the recognition that recession is almost certainly here.

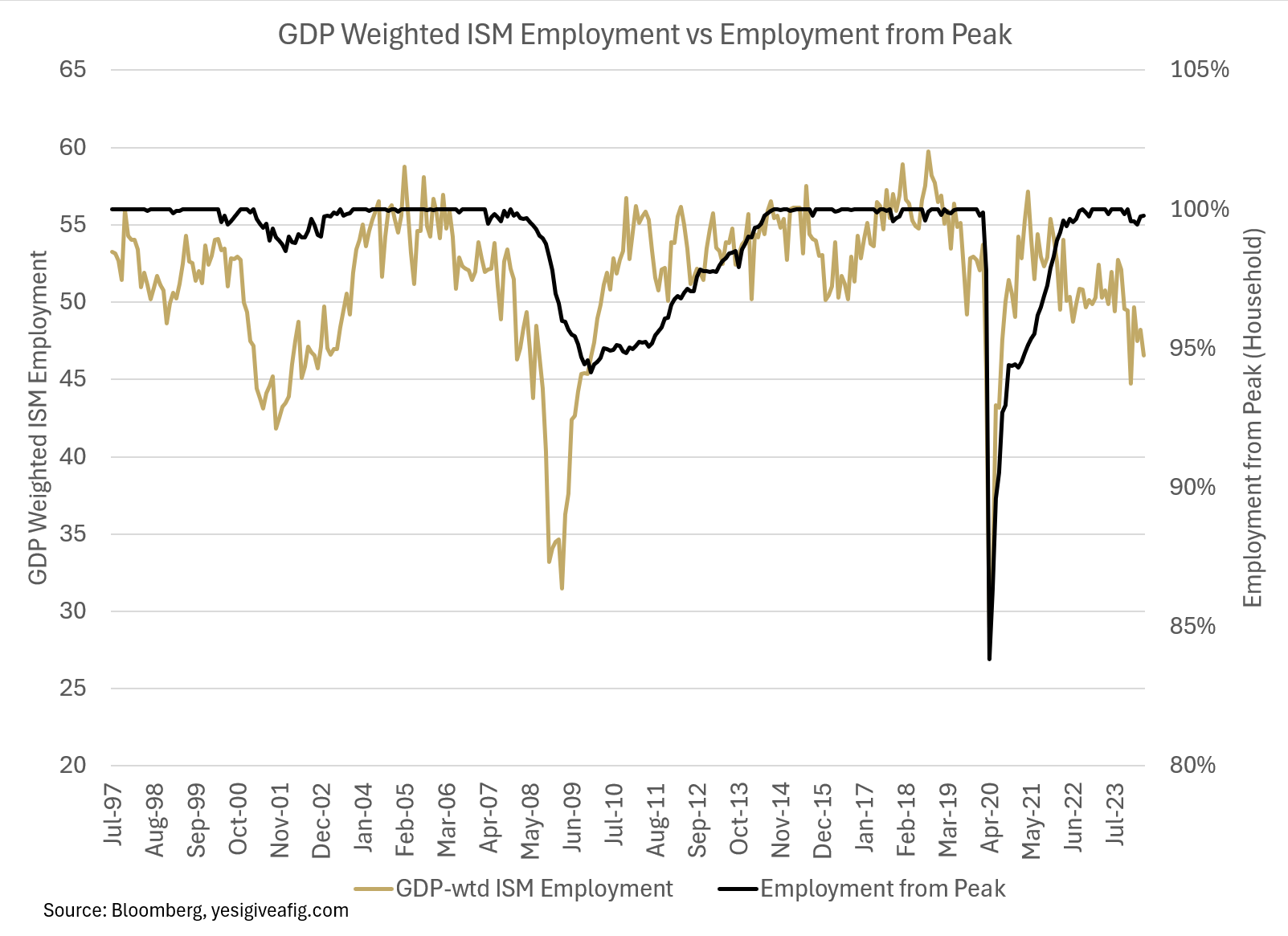

Another strong indicator of economic slowdown emerged from the weaker than expected ISM reports. Once again, the reader is free to draw their own conclusions:

To add insult to injury, the lagging JOLTs data Quit Rates also suggest that the BLS unemployment rate data is… what’s the technical term…. ahh, yes: “smoking crack.” Importantly, as we’ve highlighted in the past, we are now at the inflection point on the curve where further declines in (take your pick) job openings/quit rates/hard-plentiful/etc will lead to rapidly rising rates of unemployment.

One last, depressing, observation is that this last report on job loss was concentrated in a rise in unemployment amongst those over age 55. This is a particularly concerning statistic, because once jobs are lost for those age 50 and above, their prospects for re-employment at similar wages are low. From the Urban Institute:

Suffice it to say, across all demographic categories, the threshold for recession has been reached. The rise in unemployment has been most tame in the Prime Age cohort of 25-54. It is most obvious in the education-adjusted cohorts of “Less than Bachelor Degree” and “College Grads.”

Or perhaps presented graphically helps:

Correcting for demographic features is critical in evaluating today’s labor market. A job market that skews services, Prime Age, college-educated, and female is going to experience much lower levels of variability unemployment than one that skews towards men employed in manufacturing. Add in slow labor force growth (still true) and it is unsurprising that absolute levels of unemployment are low relative to history.

Now let’s switch to commodities. Once again, for a market that is supposedly entering a reflationary cycle, oil prices were surprisingly cooperative. As fears of Middle East conflict escalation retreat, oil prices are falling:

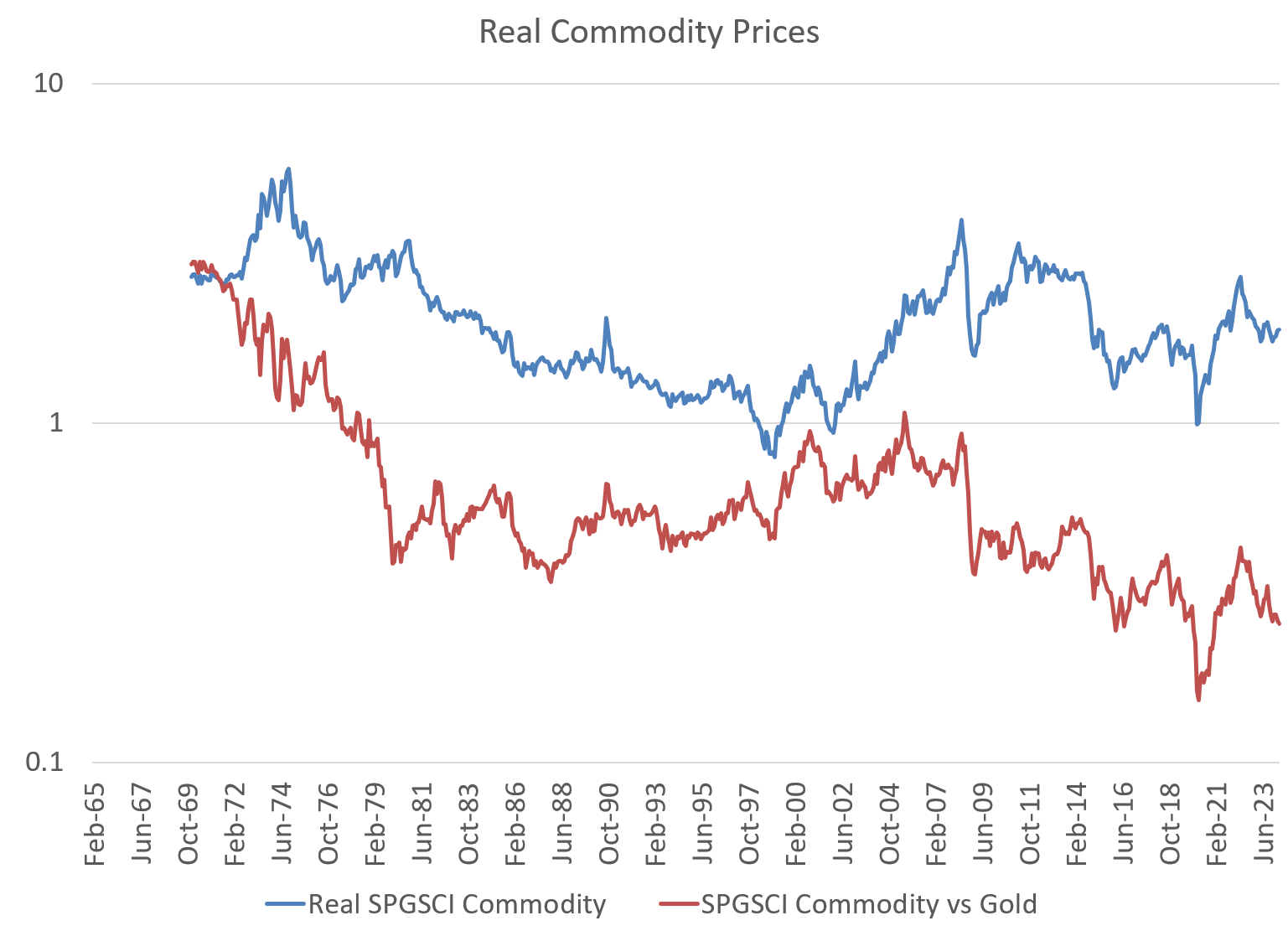

In fact, the entire commodity complex continues to broadly trend lower, especially in gold terms. As I have emphasized in the past, commodity prices are “best” measured in gold terms if our objective is to divine whether prices are being driven by economic growth (boom like the 1980-2000s) or monetary concerns. The behavior of commodities in gold suggests the most likely culprit is the latter:

This observation, of course, is grist for the mill of those arguing monetary debasement. And as I’ve accepted before, the monetary debasement is likely coming. Just not here… yet. The dollar shortage is building. We can see it in FX, where the quantity of goods that China, Japan, and Europe must sell to the US to obtain the same quantity of dollars is rising.

We can see it in Commercial Real Estate, where creditors and owners are increasingly forced to produce cash to maintain their EXISTING positions:

We can see it in rising bankruptcies for small businesses:

We can see it in rising delinquencies:

And, as we’ve been highlighting at YIGAF for over a year, this rise is most pronounced in the most vulnerable:

We’ll return to the inflationary implications in the next note, but let’s detour into the confusing micro for the remainder of this note.

The Confusing Micro

This past week, I “popped my cherry” on meme stock losses, ending up on the wrong side of Carvana’s earnings.

With options in Carvana seeing no meaningful increase in implied volatility going into earnings, I believed there was an opportunity to express a directional trade using a variant of a risk-reversal. Long three month puts, short three month calls, while buying short-dated calls to leave me “long gamma”. Why did I think this?

We had already seen Carmax (KMX) and Credit Acceptance Corp (CACC) report. My model of Carvana is a fairly simple recognition that Carvana is basically a blend of the two — an auto dealer combined with a subprime lender. Historically, Carvana’s results can be very well modeled with a mixture of the two with an R-sq of 85%. This quarter was definitely a surprise:

The behavior of subprime is critical here as the key difference between Carvana’s and Carmax’s business model is a higher fraction of financed sales — both prime and subprime. And within Carvana’s prime securitizations we were seeing losses accelerate towards attachment points at which losses result in substantive cash flow impairment:

These are the 2022 loans made at higher rates against richly priced vehicles. Now imagine the subprime… Credit Acceptance did and saw deterioration across all categories:

With deteriorating subprime conditions and poor results from peers, this appeared a layup. Unfortunately, I forgot the Phoenix factor… When I was at Royce & Associates, managing small cap assets, we always applied a Phoenix factor to handicap the risk of “misrepresentation of facts” that seemed to accompany businesses headquartered in the Phoenix region.

With no mention (or questions asked) of deteriorating credit conditions amongst lower-income borrowers on the company’s conference call, it seems fairly obvious that CVNA decided to juice sales by aggressively underwriting credit. If nobody else will offer you financing, you go where the money is to buy a car. And the seller will worry about your credit later…

Lesson learned… again.

“You asked me what I learned. I didn’t learn anything. I already knew that I wasn’t supposed to do that. So, maybe I learned not to do it again. But I already knew that.” — Stan Druckenmiller

As always, questions and comments very appreciated.

$50 Billion, $100 Billion, $50 Trillion, $100 Trillion Dollars from 2008

$50 Billion, $100 Billion, $50 Trillion, $100 Trillion Dollars from 2008